KYC – or “Know your Customer” – refers to the methods that banks and financial institutions use in order to confirm their customers’ identities, as well as the legality of their customers’ actions. These customers may be organizations or individuals.

KYC – or “Know your Customer” – refers to the methods that banks and financial institutions use in order to confirm their customers’ identities, as well as the legality of their customers’ actions. These customers may be organizations or individuals.

KYC processes are often built into the client onboarding process, and they entail all the requisite steps to ensure customers are real. Post onboarding, these processes may be sustained to continuously monitor and reduce risk since they are designed to protect financial institutions from doing business with organizations or individuals who are engaged in illegal activity such as money laundering, terrorism, or trafficking.

These vetting procedures can also provide financial institutions with better insights into their customers’ businesses and thereby enable banks to better serve their customers.

What is the meaning of a KYC check?

Banks are required to conduct a KYC check whenever a new client opens an account and periodically over time. This entails verifying that the client is genuinely who they claim to be by demanding proof of identity and proof of address. Such proof might include ID card verification, facial recognition, biometric (fingerprint) validation, and verification of documents like utility bills as proof of address.

These checks are conducted through independent and reliable sources. For example, when a corporation opens a new account, it will be required to provide social security numbers and copies of photo IDs and/or passports for employees, board members, and shareholders.

If the client fails to meet these KYC requirements, the bank may deny the request to open an account or cease the business relationship.

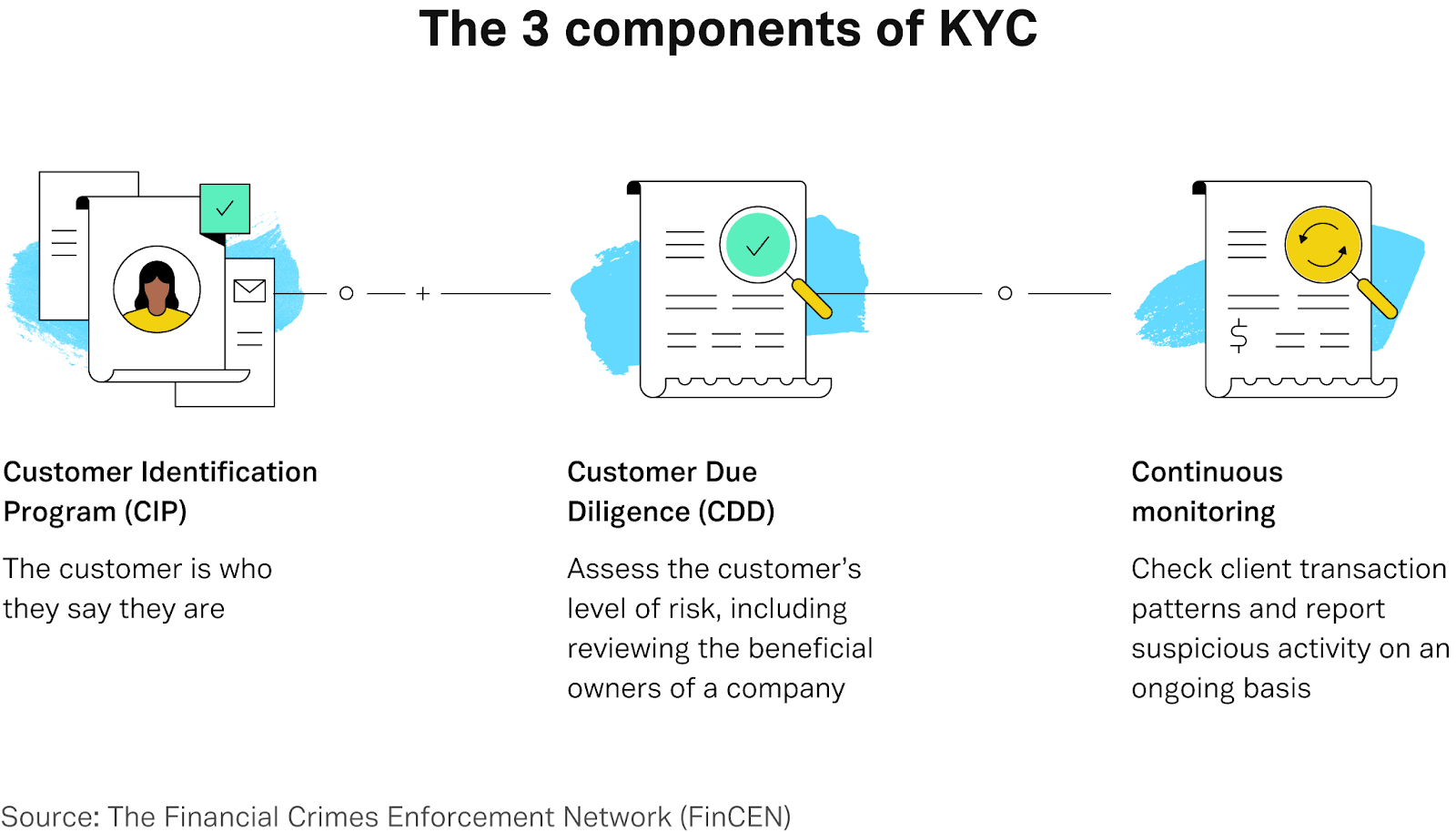

What are the three components of Know Your Customer?

There are three key components to KYC. Financial institutions must:

- Confirm the customer’s identity by obtaining four documents that contain identifying information about a client. This includes name, address, date of birth, and an identification number (such as social security or driver’s license number).

- Conduct customer due diligence (CDD), wherein the bank verifies the authenticity of these credentials and assesses the customer’s risk profile (i.e. the potential for suspicious account activity).

- Provide ongoing monitoring or enhanced due diligence (EDD). This step pertains especially to customers with higher risk profiles, meaning they pose a risk of infiltration, terrorism financing, or money laundering. In this case, additional information is collected at intervals to ensure adherence to the law and user agreement terms.

Why is KYC increasing in popularity?

KYC is increasing in popularity for 3 major reasons:

- The growing prevalence of financial crime around the world today.

- The increased number of connections between financial organizations and corporations across countries and territories.

- Pandemic-era adoption of contactless, electronic services.

The connectivity of financial institutions and corporations in the digital age means that there are more transactions (and more money traded) per day than ever before. This makes it extremely difficult to prevent illegal financial activities.

Regulators have enhanced KYC capabilities to keep pace with illicit activity. Financial institutions are legally mandated to comply with KYC and anti-money laundering statutes to limit fraud. Failure to comply with these statutes may result in heavy penalties from affected governments and institutions.

Additionally, COVID-19 pushed customers and banks to rely more heavily on digital channels and apps. Increased mobile usage encourages businesses to have a mobile-first focus and develop fully mobile user-friendly onboarding experiences. Instead of the weeks needed to complete traditional KYC processes, digital KYC can now complete such operations in seconds with a lower cost in an optimized process.

Source: ADVAM.com, Importance of knowing your customer

What is Digital KYC?

Electronic or digital KYC (or eKYC) is the term used to describe the digitalization of KYC processes. Conducting digital KYC checks (as opposed to on paper) minimizes the costs and conventional bureaucracy involved in KYC processes. eKYC can also increase customer satisfaction because of its greater efficiency and accessibility since customers can make use of these services within seconds of creating an account.

To ensure that eKYC meets the same safety standards as traditional KYC, companies must implement electronic identification processes with high levels of safety and reliability. Digital onboarding may even include video KYC (video identification) and leverage biometrics through online and mobile channels to adapt to current customer preferences. However, all eKYC processes must follow the rules outlined in AML5 or eIDAS regulations.